Variance Inflation Factor (VIF)#

Definition: VIF measures how much the variance of a regression coefficient is inflated due to multicollinearity (correlation among predictors).

If predictors are highly correlated, the coefficient estimates become unstable (large standard errors).

🔹 Formula#

For a predictor \(X_j\):

where

\(R_j^2\) is the coefficient of determination when \(X_j\) is regressed on all other predictors.

🔹 Interpretation of VIF#

VIF = 1 → No correlation with other variables.

1 ≤ VIF < 5 → Moderate correlation, usually acceptable.

VIF ≥ 5 (or 10, depending on rule of thumb) → High multicollinearity, problematic.

🔹 Why it Matters#

Multicollinearity doesn’t affect model prediction much, but it makes interpretation of coefficients unreliable.

Standard errors inflate → wider confidence intervals → coefficients may appear insignificant.

🔹 Example#

Suppose in a housing price regression:

Predictors:

sqft,bedrooms,bathrooms.sqftandbedroomsare highly correlated (bigger houses tend to have more bedrooms).VIF for

bedroomsmight be very high → its coefficient estimate becomes unstable.

👉 So, VIF is a diagnostic tool to check if your regression model suffers from multicollinearity.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from statsmodels.stats.outliers_influence import variance_inflation_factor

import statsmodels.api as sm

# Create synthetic dataset

np.random.seed(42)

n = 200

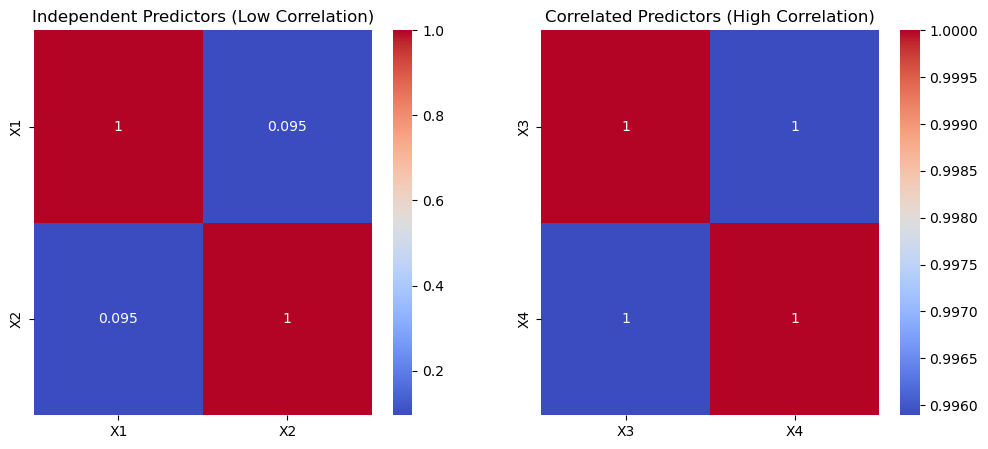

# Independent predictors (low correlation case)

X1 = np.random.normal(0, 1, n)

X2 = np.random.normal(0, 1, n)

Y = 3*X1 + 2*X2 + np.random.normal(0, 1, n)

# Correlated predictors (high correlation case)

X3 = np.random.normal(0, 1, n)

X4 = X3 + np.random.normal(0, 0.1, n) # highly correlated with X3

Y_corr = 3*X3 + 2*X4 + np.random.normal(0, 1, n)

# Put into DataFrames

df_independent = pd.DataFrame({'X1': X1, 'X2': X2, 'Y': Y})

df_correlated = pd.DataFrame({'X3': X3, 'X4': X4, 'Y_corr': Y_corr})

# Function to compute VIF

def compute_vif(df, features):

X = sm.add_constant(df[features])

vif_data = pd.DataFrame()

vif_data['Feature'] = features

vif_data['VIF'] = [variance_inflation_factor(X.values, i+1) for i in range(len(features))]

return vif_data

# Compute VIF for both cases

vif_independent = compute_vif(df_independent, ['X1', 'X2'])

vif_correlated = compute_vif(df_correlated, ['X3', 'X4'])

# Plot heatmaps of correlation matrices

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

sns.heatmap(df_independent[['X1','X2']].corr(), annot=True, cmap="coolwarm", ax=axes[0])

axes[0].set_title("Independent Predictors (Low Correlation)")

sns.heatmap(df_correlated[['X3','X4']].corr(), annot=True, cmap="coolwarm", ax=axes[1])

axes[1].set_title("Correlated Predictors (High Correlation)")

plt.show()

vif_independent, vif_correlated

( Feature VIF

0 X1 1.009136

1 X2 1.009136,

Feature VIF

0 X3 121.983031

1 X4 121.983031)